Contents

- Removal of “salary paid in the specific period” as criteria for applying JCT exemption for foreign entities

- Revision of JCT exemption for foreign entities’ first two years of business in Japan if share capital is JPY 10 million or more

- Revision of criteria for “designated newly established entities”

- Summary

Removal of “salary paid in the specific period” as criteria for applying JCT exemption for foreign entities

Treatment prior to reform:

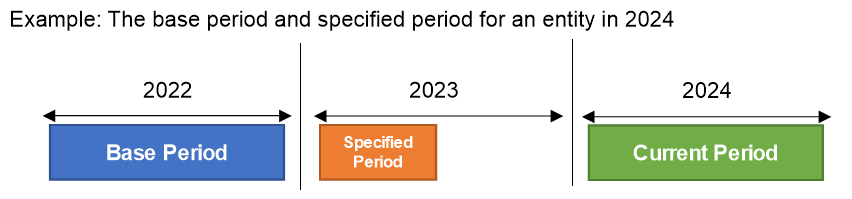

An entity may be exempt from filing or paying JCT depending on certain thresholds within the “base period” and “specified period”.

The base period is the business period two years prior to the current business period, while the specified period is the first six months of the business period prior to the current business period.

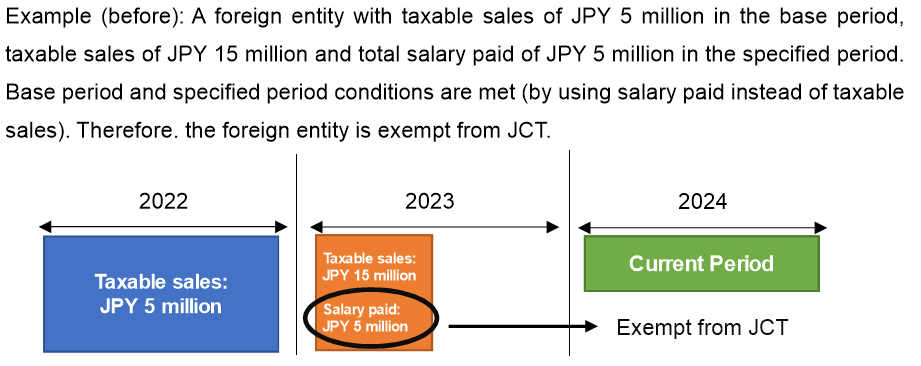

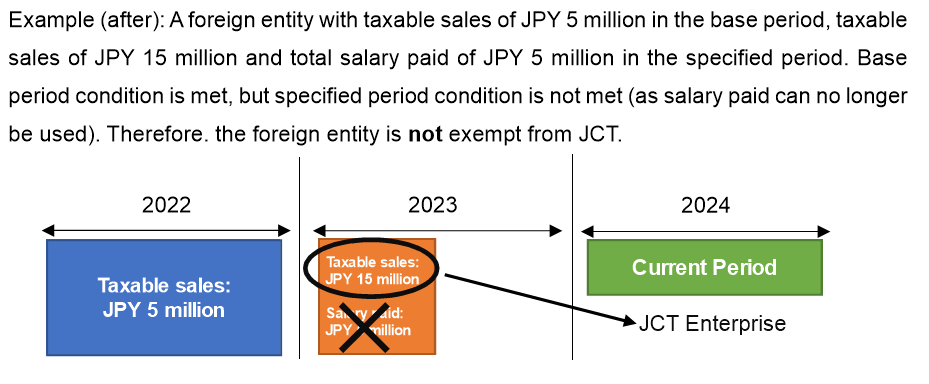

The determination of JCT exemption is based on whether taxable sales within the base period is JPY 10 million or under. If this is met, we then look at whether taxable sales within the specified period is JPY 10 million or under. If both conditions are met, the entity is exempt from JCT. In addition, for the specified period, salary paid can be used as judgement criteria instead of sales.

Treatment after reform:

The 2024 reform removes the option for foreign entities to use salary paid for the specified period test. This means that taxable sales within the base period and the specified period are now the sole determining factors for exemption applicability.

Treatment prior to reform:

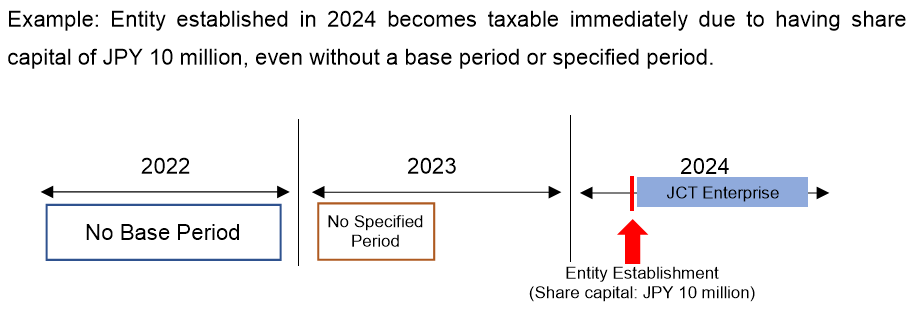

Newly established entities are deemed to not have a base period or a specified period, as it did not exist in the previous year or the year before that. Generally, this automatically enables the entity to become exempt in their first year (and second year, if specified period condition is met).

However, for newly established entities with the share capital of JPY 10 million or more, the “special provision on exemption for newly established entities” (hereinafter, “special provision”) applies, which restricts JCT exemption for these entities.

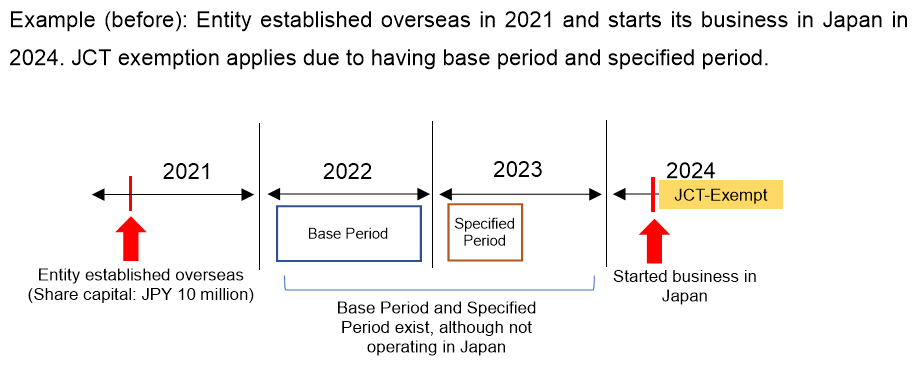

On the other hand, a foreign entity that was established more than two years ago and has recently started its business in Japan is not subject to this special provision, due to having a base period.

Treatment after reform

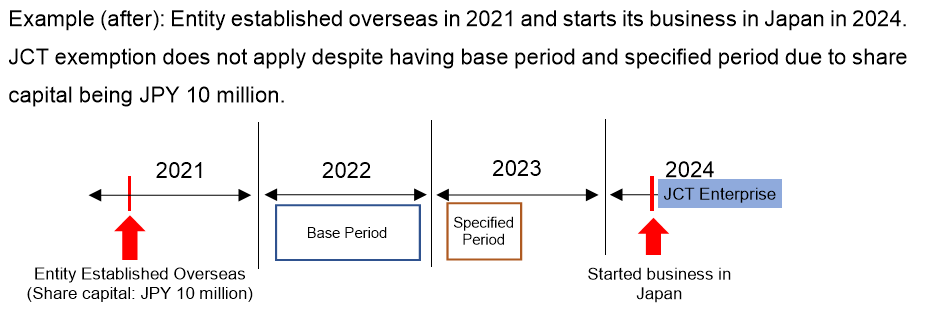

The tax reform addresses the above discrepancy in treatment between foreign entities just starting its business in Japan and newly established domestic entities. The special provision (which, as mentioned above, makes JCT exemption unavailable for newly established companies with a share capital of JPY 10 million or more) will now apply to foreign entities, even if said entity has a base period.

Revision of criteria for “designated newly established entities”

Treatment prior to reform:

A newly-established entity with a share capital of under JPY 10 million may still be classified as a JCT enterprise if they fall under the category of “designated newly established entity” (hereinafter, “designated entity”).

A designated entity is one that is controlled directly or indirectly by an entity with over JPY 500 million in taxable sales within the base period. Please note that “taxable sales” refers only to sales within Japan, which excludes most newly established entities owned by large foreign corporations from the designated entity classification.

Treatment after reform:

In addition to the above criteria, designated entities now also include those controlled directly or indirectly by an entity with over JPY 5 billion in worldwide revenue. Thus, even if the parent company have not generated sales in Japan, a newly established entity with a share capital of under JPY 10 million could still be classified as a JCT enterprise if the parent company has substantial sales overseas.

Summary

The tax reform 2024 introduced JCT-related changes relevant for companies planning to do business in Japan. Factors such as your sales, share capital, and parent company should be considered in order to understand your company’s tax position in Japan.

If you are unsure about how JCT will affect your company, please contact us through the form below.