Japanese consumption tax

The commercial sale of goods in Japan is in principal subject to consumption tax, even if the seller is a foreign company. As with domestic companies, filing and payment of consumption tax are exempt if the company meets both of the following conditions:

1. Taxable sales for the period two years prior is 10 million yen or under.

2. Taxable sales or salary paid within the first six months of the previous period is 10 million yen or under.

(For more information, please visit; https://toma.co.jp/blog/jtg/japanese-consumption-tax/)

For a company without a business establishment in Japan, filing and other tax procedures are undertaken through a tax agent. Therefore, if a foreign company is deemed to be a consumption tax enterprise due to exceeding the sales threshold, they will need to elect a tax agent who lives in Japan to complete their filing and pay taxes on their behalf.

Import consumption tax

While consumption tax arises from the sale of goods within Japan, to ensure the competitiveness of domestic producers, all goods imported into Japan are subject to import consumption tax. This applies to both corporate and individual importers.

In theory, only Japanese residents may import products into Japan. When a foreign company sells products on their website and delivers directly to consumers in Japan, the Japanese consumer acts as the importer. However, foreign companies that wish to store their products in a Japanese warehouse and sell them on a Japanese platform must somehow import the products themselves. Without a business entity in Japan, non-resident companies often utilize a forwarder or customs broker to complete this procedure. However, if the foreign company becomes a consumption tax entity, special considerations are required regarding the treatment of import consumption tax.

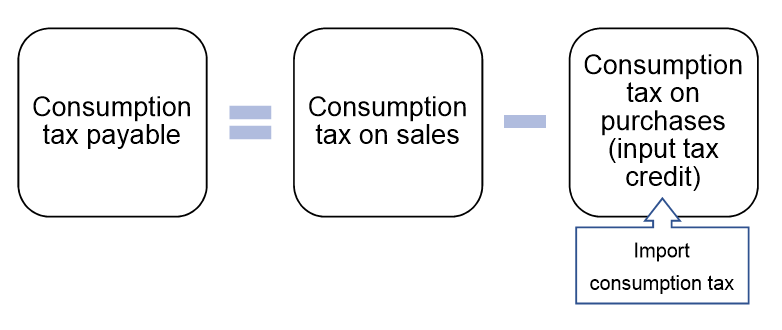

Input tax credit when importing

Like most value-added-tax systems around the world, the Japanese consumption tax system allows businesses to deduct the consumption tax on their purchases from the tax payable arising from their sales. Import consumption tax paid is included in this calculation.

However, when a customs broker imports the goods and makes the import declarations on behalf of the foreign company, they are treated as the official importer, disallowing the company from claiming import consumption tax in their filing. This issue can be addressed by utilizing an Attorney for Customs Procedure (ACP).

Attorney for Customs Procedure (ACP)

As the name suggests, the ACP can undertake certain customs procedures on behalf of the foreign company. After electing an ACP by submitting a Notification of Attorney for Customs Procedure, a foreign company can become the official importer and claim the associated the import consumption tax.

The ACP has the following responsibilities:

– Interface with the customs office on behalf of the importer

– Advise the importer of the correct information (import value, etc.) to declare

– Store the import-related documents for tax purposes

While it does not require any specific license to become an ACP, a Registered Customs Specialist license is required for ACPs engaging in import/export declarations on behalf of their clients. As such, a company may choose to elect a customs broker or a company that can liaise with a customs broker as their ACP.

Amendments in import procedures will be effected on October 1, 2023 in order to clarify and reinforce the role of ACPs. As EC transactions and imports increase, a rise in awareness and need for ACPs will likely occur.

TOMA’s Services

TOMA Consultants Group is experienced in tax matters for both foreign and domestic companies in Japan. Please reach out to us if you require a tax professional to handle your consumption tax filings, provide expert advice, or introduce you to an ACP.

On-demand Seminar Information

A Guide to the Qualified Invoice System (On-demand Seminar)

The Qualified Invoice System, starting October 2023, introduces new changes to the Japanese consumption tax rules and will affect many businesses across Japan.

The system requires a redesign of existing invoices, as well as a review of the business’ consumption tax status and suppliers.

This online seminar aims to give you an overall understanding of the Qualified Invoice System and provide measures to help you navigate the new requirements.