Background

In October 2019, Japan raised the consumption tax rate of most goods and service from 8% to 10%, with the rate for foods and drinks remaining at 8%. This multiple tax rate system introduces the risk of incorrect tax declarations, particularly for taxable purchases. The Qualified Invoice System (inboisu seido), effective from October 1, 2023, establishes new regulations surrounding input tax credits to improve accuracy and minimize tax leakage.

Consumption tax in Japan

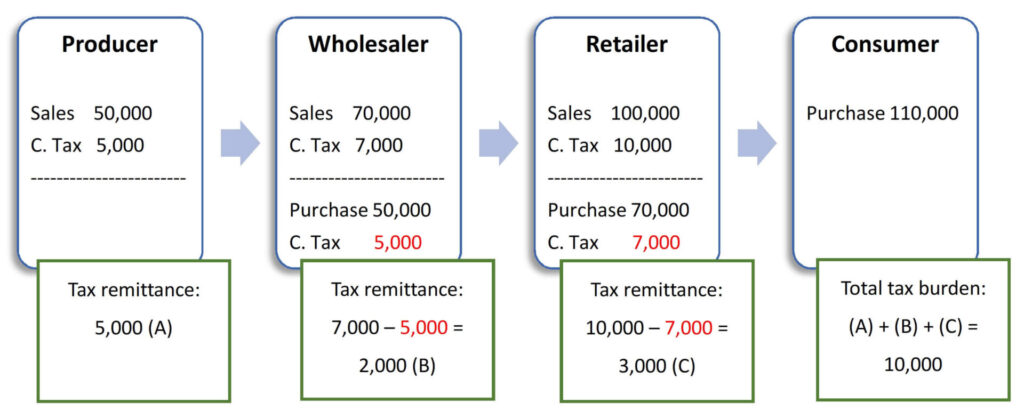

The consumption tax system in Japan levies tax on domestic sales of goods and services. Businesses along the supply chain are responsible for collecting and remitting consumption tax to the tax office, while the final tax burden falls on the consumer.

As seen in the graph above, the net tax remittance amount is the tax collected from sales minus the tax paid on purchases (as shown in red), also known as input tax credit. In order for a business to claim this amount, however, the new system requires the storage of the associated Qualified Invoice.

Qualified Invoice

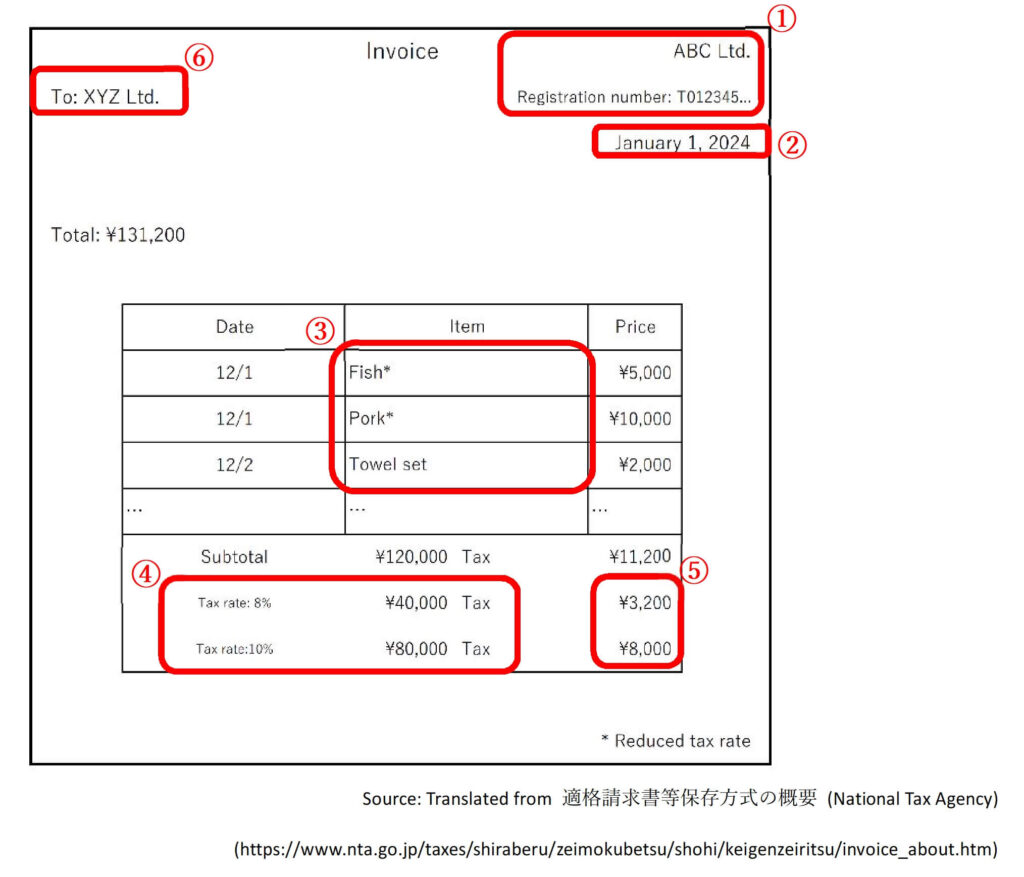

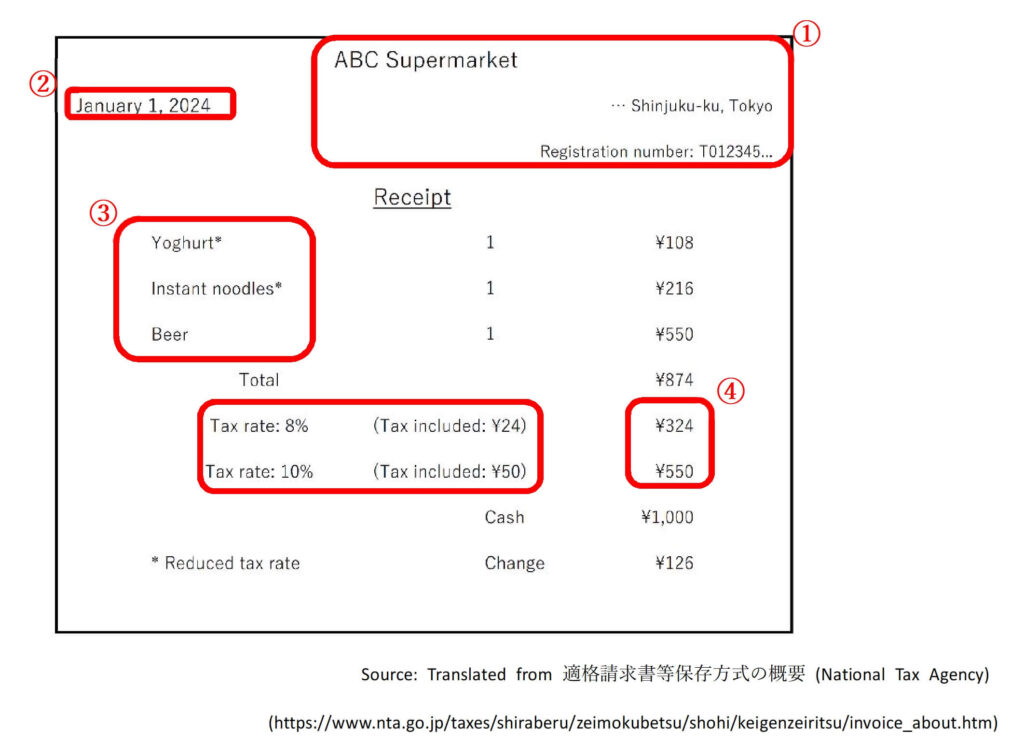

Documents such as invoices, receipts, and delivery slips, as long as they contain the required information and are issued by a Qualified Invoice Issuer, fall under the definition of Qualified Invoice. For transactions involving a large number of customers (retailers, restaurants, taxis, etc.), a Simplified Qualified Invoice, which does not require the invoice recipient name to be stated, can be issued instead.

Required information (Qualified Invoice):

1. Invoice issuer name and registration number

2. Transaction date

3. Transaction details (items under reduced tax rate stated)

4. Total price separated by tax rate (applicable tax rate stated)

5. Total consumption tax amount separated by tax rate

6. Invoice recipient name

Required information (Simplified Qualified Invoice):

1. Invoice issuer name and registration number

2. Transaction date

3. Transaction details (items under reduced tax rate stated)

4. Total price separated by tax rate

5. Total consumption tax amount OR applicable tax rate separated by tax rate

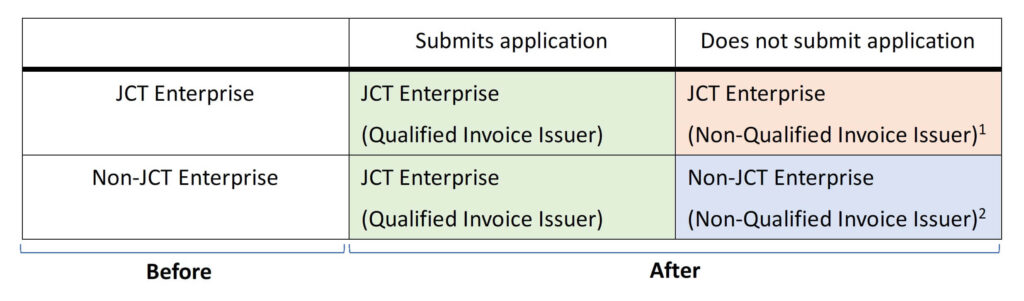

Qualified Invoice Issuer

In addition to the requirements laid out above, a document must be issued by a Qualified Invoice Issuer to be a Qualified Invoice. In order to become a Qualified Invoice Issuer, an application form must be submitted by the business, whether they are a JCT enterprise or not (See our blog here about JCT enterprises). Furthermore, if a non-JCT enterprise applies to become a Qualified Invoice Issuer, they will automatically become a JCT enterprise.

¹It is possible for a JCT enterprise not to apply to become a Qualified Invoice Issuer. However, as JCT enterprises must file consumption tax returns regardless, there are no drawbacks to becoming one.

²A non-JCT enterprise may choose to remain such by not applying to become a Qualified Invoice Issuer. However, as explained previously, invoices not issued by a Qualified Invoice Issuer cannot be used to claim input tax credits. This is disadvantageous for the business’ customers and may result in negotiations in price and even contract cancellations. It is necessary for a non-JCT enterprise to weigh up the costs and benefits of becoming a JCT enterprise.

A business that wishes to become a Qualified Invoice Issuer as of October 1, 2023 must apply before March 31, 2023. Once the application has been approved, the business will be given a registration number (otherwise known as tax number). This number must be stated on any Qualified Invoices issued by the business, and is searchable on the National Tax Office’s website (https://www.invoice-kohyo.nta.go.jp/).

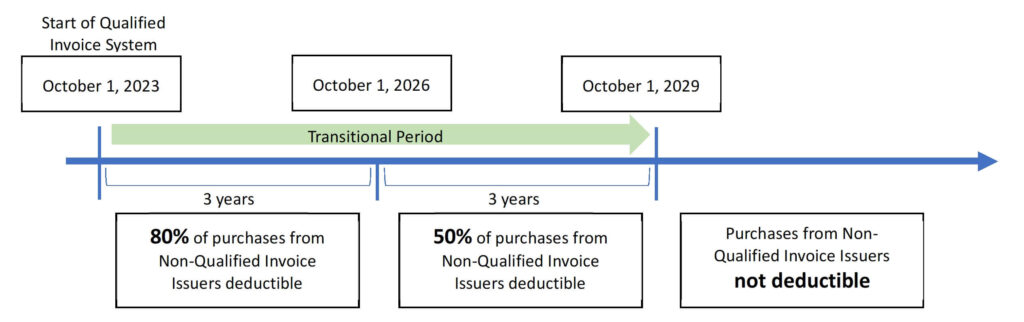

Transitional measures

The Qualified Invoice System applies from October 1, 2023. However, there will be a transitional period from the start of the system until October 1, 2029, during which a portion of purchases from Non-Qualified Invoice Issuers will be tax deductible.

Furthermore, if a Non-JCT Enterprise applies to become a Qualified Invoice Issuer during the transitional period, they can become a JCT Enterprise immediately on the day the application is approved.

On-demand Seminar Information

Corporate Taxation in Japan (On-demand Seminar)

Companies operating in Japan are faced with a wide array of taxes and compliance procedures. The complexity is further compounded by the lack of reliable, easy-to-understand English resources.

This online seminar aims to give you a comprehensive overview of the Japanese corporate tax system, covering the various tax types, calculation and filing procedures, and other regulatory requirements.

>>Click here for seminar details and registration

A Guide to the Qualified Invoice System (On-demand Seminar)

The Qualified Invoice System, starting October 2023, introduces new changes to the Japanese consumption tax rules and will affect many businesses across Japan.

The system requires a redesign of existing invoices, as well as a review of the business’ consumption tax status and suppliers.

This online seminar aims to give you an overall understanding of the Qualified Invoice System and provide measures to help you navigate the new requirements.

>>Click here for seminar details and registration

TOMA’s services

TOMA Consultants Group can assist you with the following:

– Application to become a JCT enterprise or a Qualified Invoice Issuer

– Filing of consumption tax returns

– Assessment of whether becoming a JCT enterprise would be right for you

– Assessment of the best taxation method to use

– Other related consultation

Please contact us for a free consultation on how we can best support your business in Japan.