Question 1: What are the basics of the Qualified Invoice System?

The Qualified Invoice System is a consumption-tax-related system that took effect in October 2023. In order to understand its implications, we must first understand the consumption tax system in Japan.

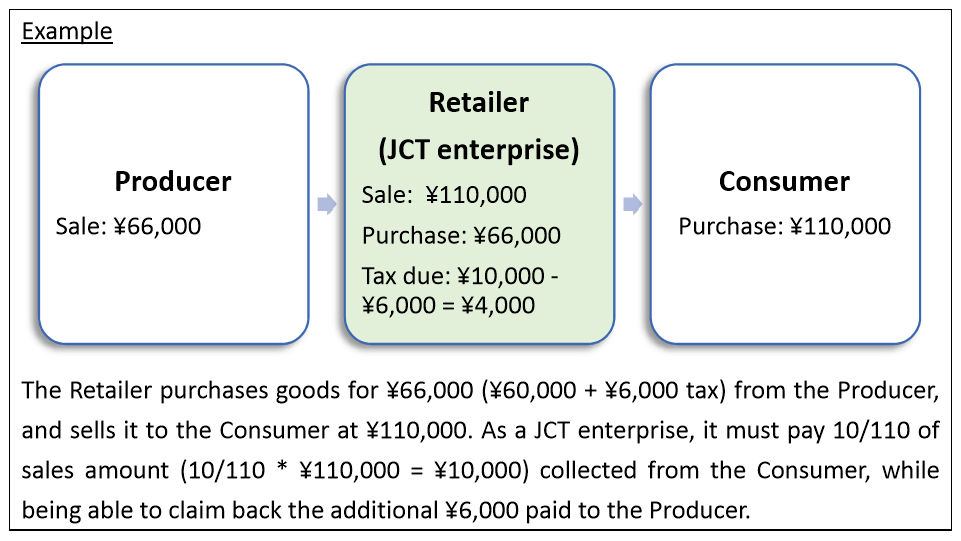

Japan collects 10% (or in some cases 8%) in tax from “consumption tax enterprises” (JCT enterprises) on their sales. In turn, the JCT enterprise adds 10% or 8% to its sales price to customers, essentially passing the tax burden down to consumers.

Similarly, when a JCT enterprise makes a purchase itself, it also pays extra on consumption tax. Unlike regular consumers, however, it may claim a deduction (known as input tax credit) on this tax paid.

The Qualified Invoice System creates new conditions surrounding this deduction. It stipulates that in order to claim the input tax credit, the business must receive a Qualified Invoice, which is an invoice that meets certain standards and is issued by a Qualified Invoice Issuer. Furthermore, only JCT enterprises may become Qualified Invoice Issuers.

In effect, this means that JCT enterprises will be more inclined to purchase from Qualified Invoice Issuers (and thus, JCT enterprises) in order to reduce their tax burden. This can also result in non-taxable businesses opting to become a JCT enterprise to accommodate its business clients.

Question 2: I am a business owner operating in Japan with local clients. Do I have to become a Qualified Invoice Issuer?

Registration to become a Qualified Invoice Issuer is optional. The following points should be considered before becoming one.

Pros:

- Allows your business clients to claim input tax credit on their purchases from you.

- Registration may be required in order to sell on certain sales platforms.

- If wishing to become a JCT enterprise, the business can become one during the business year by registering as a Qualified Invoice Issuer, as opposed to waiting until the next business year. (Note: This only applies during the transitional period until September 2029.)

Cons:

- If previously tax-exempt, will now need to start paying consumption tax on sales.

- If previously tax-exempt, will now need to prepare and file consumption tax returns.

- Will need to review existing invoices and receipts to make sure they are Qualified Invoices.

Question 3: Can I become a Qualified Invoice Issuer immediately, i.e. in the middle of the financial year?

As a JCT enterprise, you may apply for Qualified Invoice Issuer status in the middle of the financial year and become one as soon as the application is received.

As a tax-exempt enterprise, within the transitional period until September 2029, you may also become a Qualified Invoice Issuer (and thus, a JCT enterprise) in the middle of the financial year. In this case, you must state your desired registration date on the application form. This date must be at least 15 days after the date of application.

Question 4: I have applied to become a Qualified Invoice Issuer but have not yet received my registration number. How do I issue tax deductible invoices in the meantime?

Below are acceptable measures you may take during this period:

- Issue an invoice without a registration number, inform your customer, and reissue a Qualified Invoice at a later date.

- Issue an invoice without a registration number, inform your customer, and issue a separate notice about your registration number at a later date.

- (For retailers) Issue an invoice without a registration number, inform your customers, and announce your registration number at a later date on your website or inside your store.

Question 5: What do I need to know regarding employee reimbursement?

Companies generally wish to claim input tax credits on travel expense reimbursed to their employees. However, as employees are unable to issue Qualified Invoices, an exemption is in place where travel expenses such as accommodation, per diem, and transportation costs deemed “typically necessary” will not require an associated Qualified Invoice.

For other expenses reimbursable to the employee, such as meal, stationary, or telecommunication expenses, please ensure that the Qualified Invoice is addressed to the company, and not to the employee. If the Qualified Invoice is addressed to the employee, the company must receive a separate reimbursement statement from the employee.

Simple Qualified Invoices, which is a simplified version of Qualified Invoice issuable by retailers, restaurants, and other businesses with an unspecified number of customers, may be addressed to the employee provided that the individual is a recorded employee of the company. In this case, a reimbursement statement is not required.

TOMA’s services

TOMA is experienced in tax matters for both companies and individuals. Please reach out to us if you require tax consultation or tax filing services.

Please get in touch with us through the Contact Us tab below.