As an employer in Japan, you are required to make various deductions to your employees’ salary before their income tax is calculated. These deductions are collectively known as social insurance (shakai hoken) and aim to support the livelihood and wellbeing of employees.

Insurances that compose the social insurance system:

1. Pension insurance

2. Health insurance

3. Long-term care insurance

4. Employment insurance

5. Workers’ accident compensation insurance

Every month, the employer is responsible for paying the employee contributions for pension insurance, health insurance, and long-term care insurance, as well as the portion borne by the employer, to Japan Pension Service.

Meanwhile, employment insurance and workers’ accident compensation insurance (together known as “labor insurance”) are paid once a year to the Labor Bureau. In addition, although employment insurance contains an employee portion, worker’s accident compensation insurance is paid for entirely by the employer.

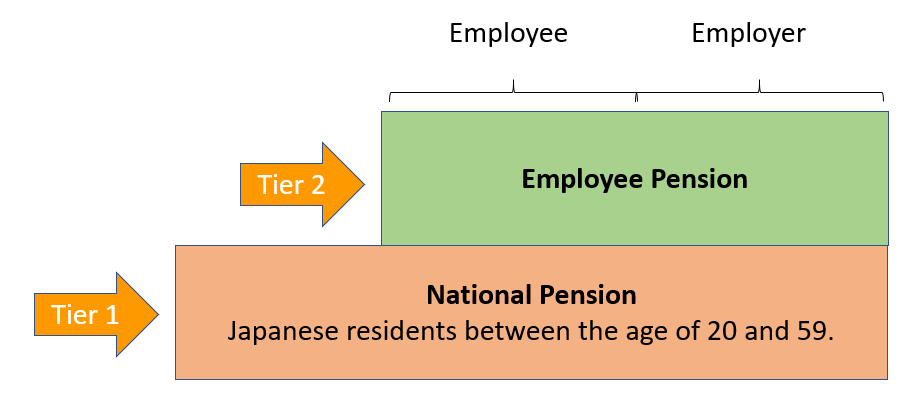

Pension insurance

The Japanese pension system comprises two tiers: National Pension and Employee Pension. National Pension is paid by all Japanese residents aged 20-59. Meanwhile, Employee Pension is paid by salaried workers on top of National Pension. Even after the age of 60, enrollees must continue to pay Employee Pension if they continue working and fulfill the social insurance conditions, however, payments will no longer be required from the age of 70. Half of Employee Pension is paid by the company and half by the employee.

Health insurance

Japanese health insurance is mandatory for all residents of Japan. This insurance entitles the enrollee to pay only a portion of medical costs (from 10% to 30%, depending on the age of the enrollee) as well as benefits such as maternity allowance, accident and sickness allowance, and reimbursement for high-cost medical care. Monthly contributions are calculated based on a percentage of the enrollee’s salary (percentage varies by prefecture, e.g. 9.81% in Tokyo), half of which is paid by the employer. From the age of 75, even if the enrollee works for a company, they will be transferred to the Medical Insurance System for the Latter-Stage Elderly.

Long-term care insurance

Mandatory contributions towards long-term care insurance start at age 40. Generally, the enrollee may access the benefits of this insurance from the age of 65. However, it is also available to those between the ages of 40 and 64 if they require long-term care due to an aging-related illness (terminal cancer, rheumatoid arthritis, etc.). Like health insurance, contributions are calculated based on the enrollee’s salary, half of which is paid by the employer.

Employment insurance

Employment insurance is a mandatory program that provides monetary support during unemployment or leaves of absence. The system includes various types of allowances depending on the enrollee’s circumstances, one of which being the “basic allowance,” an unemployment benefit calculated as a per-day allowance (based on previous salary) paid over a specified time period (between 90 and 360 days depending on cause of unemployment and period enrolled). Employment insurance premiums are calculated as a percentage of salary, with the employer paying a larger portion.

Workers’ accident compensation insurance

The other part of labor insurance is the workers’ accident compensation insurance. This insurance compensates the employee in cases of illness and injury (or their family in the case of death) during work or commute. Unlike the other social insurances, premiums for this insurance are covered entirely by the employer.

It is important to note that directors and executives are generally not eligible for employment insurance and workers’ accident compensation insurance, as their contractual relationship with the company is an engagement agreement and not a labor contract. However, directors may become eligible for workers’ accident compensation insurance through a system called “Special Enrollment” if certain requirements are met.

TOMA’s services

An employer in Japan is not only responsible for calculating salary and bonuses for its employees, but also the enrollment and management of the aforementioned social insurance system. At TOMA Consultants Group, we have a dedicated team of Labor and Social Security Attorneys to assist you in all aspects of payroll. For more information, please get in touch with us through the link below.