Contents

Background of the Tax Revisions

The basic income tax deduction in Japan had remained a fixed amount, which became problematic as inflation pushed up the effective tax burden. However, this issue remained largely unnoticed during the country’s long period of deflation. With the recent trend of rising prices, particularly for essential goods, the tax burden on individuals has increased. In response, the income tax deduction has been revised upward to better reflect current economic conditions.

Basic Income Tax Deduction

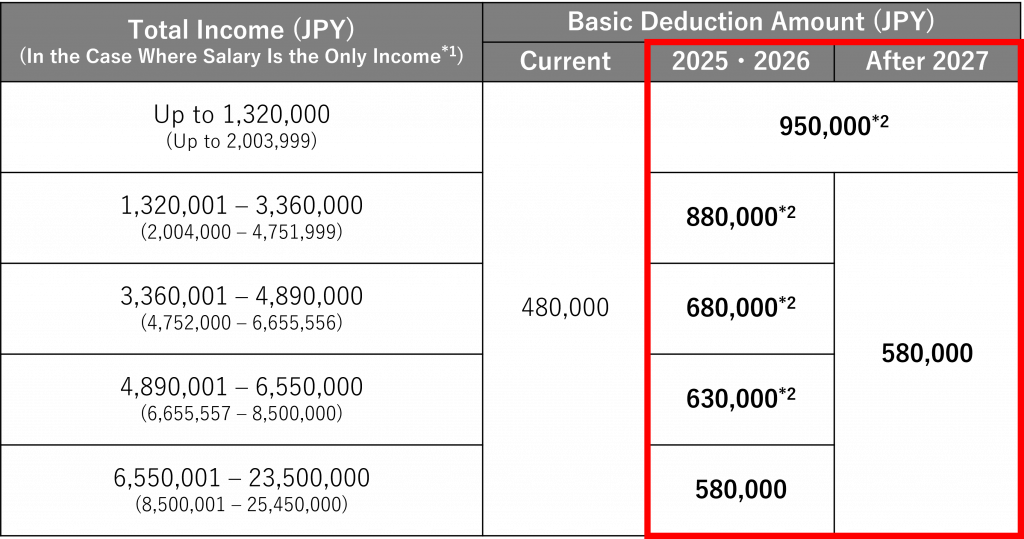

In consideration of rising prices, the maximum basic income tax deduction has been increased by ¥100,000—from ¥480,000 to ¥580,000. Furthermore, to reduce the tax burden on low- and middle-income earners, an additional deduction of up to ¥370,000 has been granted based on income levels as follows:

*1. If there are special expense deductions or income adjustment deductions, the amounts in the table may differ.

*2. For total taxable income amounts of ¥6.55 million or less, additional amounts of ¥370,000, ¥300,000, ¥100,000, and ¥50,000 will be added to the basic deduction of ¥580,000 depending on the income bracket. These additional deductions apply only to residents.

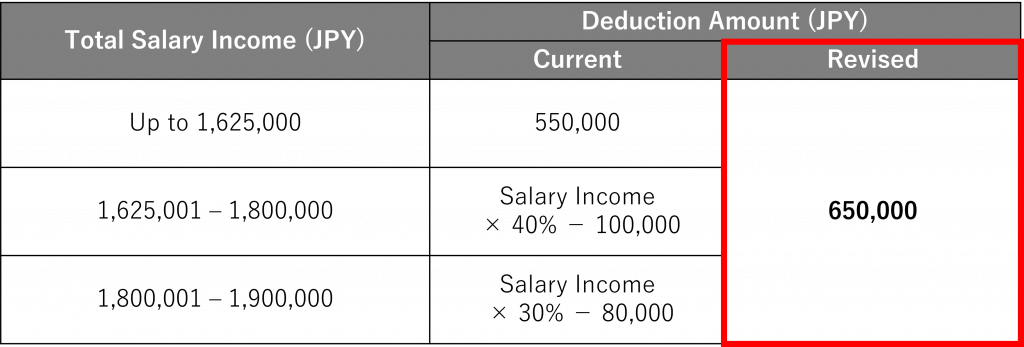

Employment Income Deduction

In response to inflation and the issue of individuals limiting their working hours due to income caps, the minimum deduction amount has been raised by ¥100,000—from ¥550,000 to ¥650,000 as follows:

New:Special Deduction for Specified Relatives

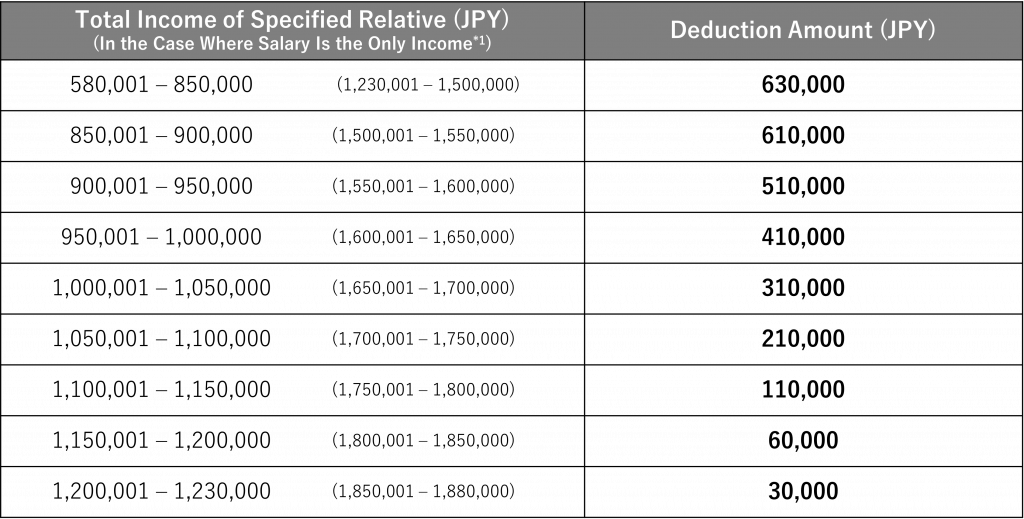

This special deduction was established in response to the current labor shortage, particularly to address the issue of university students reducing their working hours to remain within income thresholds. Parents who have a “Specified Relative” (see note below) may deduct up to ¥630,000 per specified relative from their taxable income. If the specified relative’s total income exceeds ¥850,000, the deduction amount is gradually reduced as follows:

*1. If there are special expense deductions or income adjustment deductions, the amounts in the table may differ.

Note: “Specified Relatives” are family members aged 19 or older but under 23 who live in the same household as the taxpayers or are supported financially by them. This excludes spouses, individuals receiving a salary as family employees of a blue return filer, and white return filers. Foster children are also included.

If the relative’s total income is ¥580,000 or less, they are not eligible for this special deduction but may instead qualify for the standard dependent deduction. Relatives aged 19 to under 23 are classified as “special dependent relatives,” for whom the standard dependent deduction is ¥630,000.

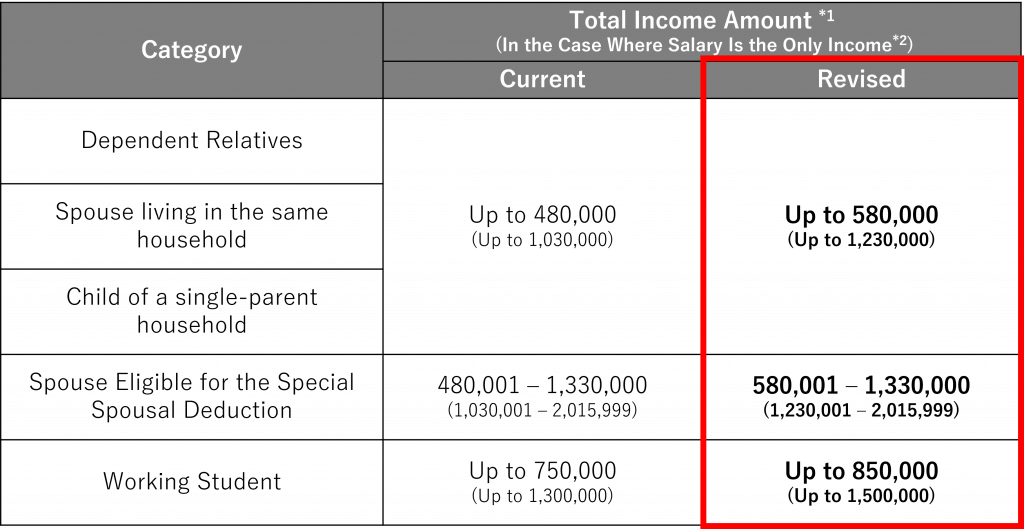

Income Requirements for Dependent Relatives

Following the revision of basic income tax deduction, the income eligibility threshold for dependents to qualify for related tax deductions has been raised from ¥480,000 to ¥580,000 as follows:

*1. For a child of a single-parent household, it refers to the total income after deductions.

*2. If there are special expense deductions or income adjustment deductions, the amounts in the table may differ.

Important Notes

As mentioned at the beginning, the revisions to the basic income tax deduction and related changes will take effect on December 1, 2025, and will apply for income tax from 2025 onwards. Accordingly, year-end tax adjustments and other withholding tax procedures carried out in December 2025 and beyond will be affected by these changes. (There will be no changes to withholding procedures through the end of November 2025.)

For year-end adjustments, for example, employees who have newly eligible dependents or who wish to claim the newly established “Special Deduction for Specified Relatives” will be required to submit the designated forms. Payroll personnel will need to calculate the year-end adjustments based on the revised amounts for the basic deduction, employment income deduction, and other relevant items.

These changes may cause concern for some company personnel in charge of payroll and tax procedures.

At TOMA Consultants Group, we provide prompt, reliable support from our tax and labor specialists.

If you have any questions or concerns, please contact us through the form below.