Contents

Overview

The treatment of capital gain under Japanese tax law differs according to the asset being transferred and the period of ownership.

Assets subject to capital gains tax include, but is not limited to, the following:

・Land and buildings

・Leasehold rights

・Stocks and other securities

・Precious metals and gems

・Paintings and antiques

・Machinery and equipment

・Golf membership

・Copyright

Assets for everyday use, such as furniture, vehicles used for commuting, and items of clothing, are excluded. Precious metals and gems, paintings, etc. under 300,000 yen are deemed as “assets for everyday use.”

Capital gain is generally calculated as follows:

Capital gain = Income earned – (acquisition cost + cost of transfer)

Comprehensive taxation

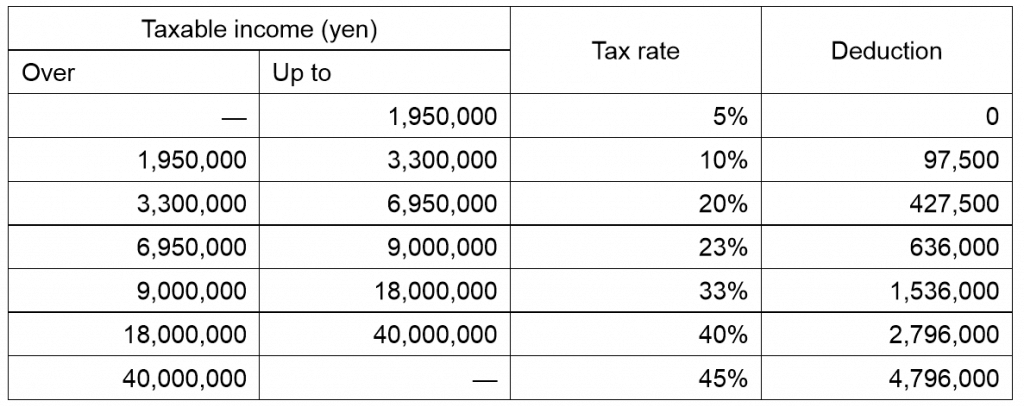

Capital gain from the transfer of assets other than land, buildings, and securities is subject to comprehensive taxation. This means that the capital gain is aggregated with other income types such as employment income, business income, and rental income, before applying deductions and being taxed according to the table below:

Capital gain that is subject to comprehensive taxation is eligible for a special deduction of up to 500,000 yen. Furthermore, capital gain on long-term assets (assets held for more than 5 years) is halved before being added to comprehensive income.

Capital gain on land and buildings

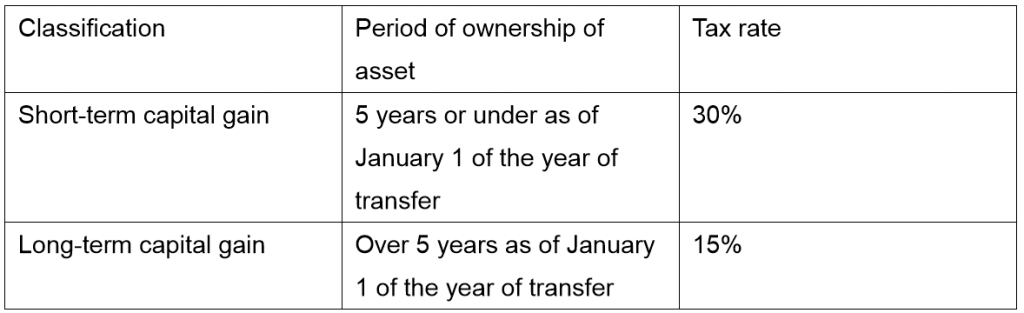

Capital gain from the transfer of land and buildings is subject to “separate taxation.” Unlike comprehensive taxation, separate taxation applies a flat tax rate to the total capital gain in each classification. The classifications and their applicable tax rates are below:

Special tax rates apply in situations such as property for residential use held for over 10 years. Furthermore, special deduction may apply in cases such as transfer of residential use property and transfer of assets for expropriation.

Capital gain on stocks and other securities

Like capital gain from the transfer of land and buildings, capital gain from transfer of stocks and other securities is also subject to separate taxation. Transfer of stocks and other securities is divided into the following classifications: 1) listed stocks (includes listed stocks, publicly offered investment trusts, government bonds, etc.) and 2) unlisted stocks (securities not classified under “listed stocks”). Losses from one classification cannot be used to offset the profit of another classification.

Both listed and unlisted stocks are subject to income tax of 15%.

TOMA’s services

TOMA is experienced in tax matters for both companies and individuals. Please reach out to us if you require tax consultation or tax filing services.

Please get in touch with us through the Contact Us tab below.