Contents

Purpose of Exit Tax

Under Japanese tax law, Japanese residents are in principal subject to income tax on their worldwide income, including capital gains. In other words, individuals who wish to sell their assets can minimize or avoid capital gains tax by moving to a country with little or no tax on capital gains before selling their assets, as they are no longer a tax resident of Japan.

Exit Tax is designed to address this by imposing income tax on individuals at or around the time they exit the country, effectively treating them as if they have sold their assets before departure.

Individuals Subject to Exit Tax

Individuals who exit Japan to reside abroad and meet the following conditions are subject to Exit Tax:

– Own over 100 million yen in subjected assets*, both in Japan and overseas

– Have had a domicile or residence in Japan for over 5 of the last 10 years**

* Subjected assets: Stocks, investment trusts, bonds, equity in anonymous partnership agreement, outstanding margin transactions, outstanding when-issued transactions, outstanding derivative transactions, and others.

** Excluding period of stay under a status listed in Table I of the Immigration Control and Refugee Recognition Act.

Procedures

Individuals subject to Exit Tax who leave Japan to reside abroad are deemed to have sold their assets at the value as of the following dates:

1. If tax return is filed after leaving Japan: Value of assets on date of departure

2. If tax return is filed before leaving Japan: Value of assets three months before schedule date of departure

For outstanding transactions or derivatives, the taxable value is determined assuming the asset was settled on the above dates.Depending on the type of asset, the income shall be deemed to be capital gains, business income, or miscellaneous income.

Subjected individuals must file an income tax return and pay the application tax by one of the following dates:

1. If a “Notification of Tax Agent” was submitted: By March 15 of the year following departure (standard tax filing deadline).

2. If a “Notification of Tax Agent” was not submitted: By the day of departure.

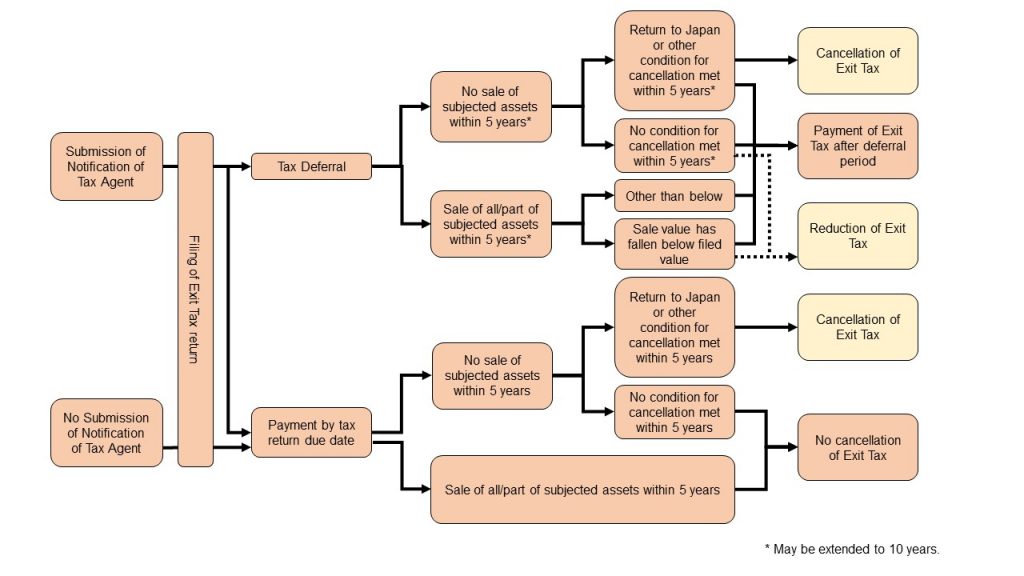

Deferral of Exit Tax

A five-year (or, if extended, ten-year) deferral on payment of Exit Tax is available for individuals who have submitted a Notification of Tax Agent before leaving Japan. The following steps are required to apply this deferral:

1. File an income tax return, together with required attachments, and provide collateral (such as real property, bonds, approved stocks, etc.) equal to the amount of tax duty and interest by the filing deadline.

2. Submit notification of continuing application of deferral every year thereafter by the filing deadline.

3. If wishing to extend past 5 years, submit a notification of extension before 5 years have passed since leaving Japan.

During the tax deferral period, if all or part of the subjected assets are sold, settled, or gifted, income tax associated with that portion must be paid within four months of sale, etc.

Tax Reduction/Cancellation Measures

In addition to tax deferral, tax reduction or cancellation measures are also available under certain circumstances after tax filing.

Firstly, if the individual continuously owns the subjected assets and returns to Japan within five years of departure, they may apply to have their Exit Tax cancelled (or refunded in the case where it was paid before departure). In this case, a request for tax correction or amended tax return must be submitted within four months of their return to Japan.

The same measure is available if the subjected assets are gifted to a Japanese resident, or if a resident inherits the subjected assets due to the death of the tax filer.

Tax reduction measures are also available in circumstances such as a reduction in value of the subjected assets upon its transfer, settlement, or limited inheritance, reduction in value of subject assets upon expiration of the tax deferral period, or the occurrence of double taxation due to transfer of the subjected assets.

Gifting or Bequest of Subjected Assets to a Non-resident

Exit Tax also applies in the below situations where the individual does not leave Japan:

1. Gifting of subjected assets to a non-resident

2. Inheritance of subjected assets by a non-resident

This is because gifting and inheritance effectively enable the individual to transfer the assets overseas without triggering capital gains tax.

Subjected individuals and assets are the same as described in the previous sections. Tax deferral and reduction measures similar to the previous section are also applicable.

Flowchart

TOMA’s Services

TOMA is experienced in international tax matters for individuals as well as companies. Please reach out if you require tax consultation or tax filing services.