Contents

Withholding income tax

Like many countries, Japan employs the tax withholding system for many types of income in order to reduce tax evasion and tax collection costs, as well as ensuring a steady stream of tax revenue for the government. For salary workers, which compose roughly 90% of Japan’s working population (Statistics Bureau of Japan, 2022), the tax withholding system requires their employers to withhold a portion of salary as income tax. In addition to salary, income such as public pension, remuneration for lawyers and tax accountants, compensation for articles and translations, etc. also fall within the scope of withholding tax.

Generally, employers are obligated to pay withholding income tax for the current month to the tax office by the 10th of the subsequent month. However, businesses with nine or less employees can submit an “application for payment of withholding income tax semiannually,” which allows them to pay the withholding income tax only twice a year: once in July and once in January (subsequent year).

Year-end adjustment

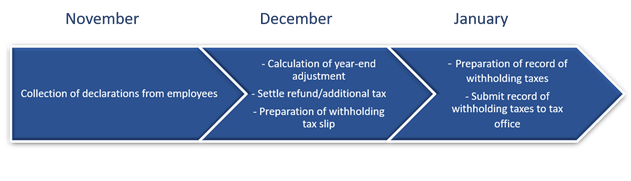

At the end of every year, employers settle the discrepancy between their employees’ withheld tax amount and the actual taxable amount through a process called the year-end adjustment (nenmatsu chosei). The discrepancy arises because the monthly withheld amount is calculated assuming a fixed salary amount throughout the year and no changes to dependents. The deadline for year-end adjustment is January 31 of the subsequent year. However, many companies complete this process before the end of the year so that refunds/additional taxation are reflected in December’s salary payment.

The year-end adjustment process requires the employer to collect various declarations from the employee in order to calculate deductions. This includes changes to dependents, spouse’s income, and insurance payments. Once calculations are complete, the employer prepares the withholding tax slip (gensen choshu hyo), of which one copy is to be handed to the employee and one copy submitted to the tax office.

Record of withholding taxes

Every year, companies are required to submit documents collectively known as record of withholding taxes (hotei chosho) to the tax office. These documents show the payments made to employees, professionals, landlords, etc. throughout the calendar year, and is used by the tax office to corroborate the payment receiver’s tax declarations.

Documents included in record of withholding taxes

– Withholding record total table

– Withholding tax slips (for salary)

– Withholding tax slips (for retirement income)

– Reports of payment of remuneration, charges, contract money, and monetary rewards

– Reports of payment of real estate rentals

– Reports of payment for transfer of real estate

– Reports of payment for real estate intermediary fees

– Other reports of payment depending on payment type

Rules regarding which payments are to be recorded differ between the type of report. It may be necessary to consult or outsource this procedure to a tax accountant to ensure the record of withholding taxes is completed correctly.

Overview of year-end adjustment and record of withholding tax procedure

TOMA’s services

TOMA Consultants Group has a dedicated team of Labor and Social Security Attorneys and Certified Tax Accountants to assist you in matters regarding withholding tax, payroll, and tax document submissions. For more information, please get in touch with us through the link below.